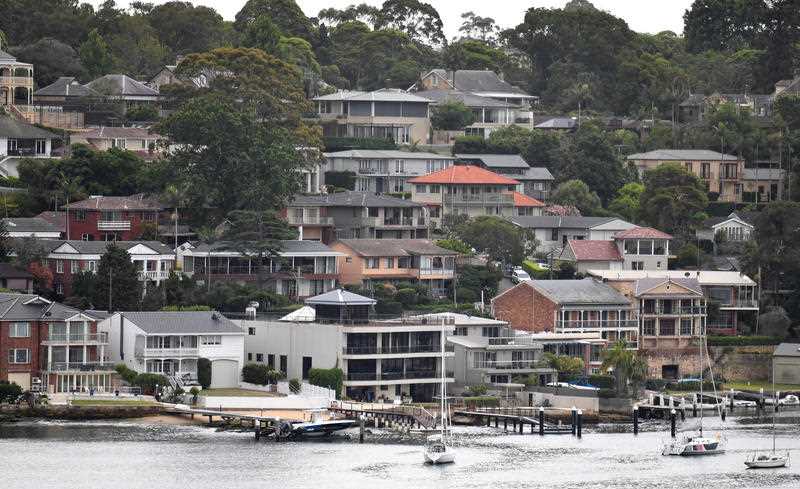

The value of new mortgages slipped another 2.1 per cent in January, marking Australia's largest annual decline since the global financial crisis.

The value of dwelling commitments excluding refinancing slipped to $17.12 billion in January, according to seasonally adjusted figures released on Tuesday by the Australian Bureau of Statistics. That made for a 12-month decline of 20.6 per cent, with the total number of owner-occupier mortgage commitments falling 2.6 per cent over the month and 13.6 per cent over the year to 47,407. "The pace of declines in housing finance eased in January from the sharp declines in December, but the trend remains very weak, with a positive turn unlikely in the near term," ANZ economists Jack Chambers and David Plank said. "Further improvements in housing affordability or a significant loosening in lending standards (which is unlikely) would be the necessary precursors to an improvement in finance and the housing market overall." House prices in most capital cities have fallen - by more than 10 per cent in Sydney from their 2017 peaks - as lenders tighten the flow of credit amid regulatory intervention and the harsh light of the royal commission. "Weaker lending for dwellings again drove much of the overall fall in lending to households, with further falls in lending for investment dwellings and for owner-occupier dwellings in January," ABS chief economist Bruce Hockman said. "Reflecting the impact of both supply and demand side factors, new lending for dwellings is down over 20 per cent from January 2018, the largest through the year decline since late 2008." The biggest monthly fall in the number of owner-occupier commitments was the 9.5 per cent drop for newly built homes. In dollar terms, owner-occupier dwellings excluding refinancing fell 1.3 per cent to $12.45 billion, taking the annual decline to 17.1 per cent. New investor loans fell 4.1 per cent in January - and 28.6 per cent over 12 months - to $4.67 billion. Total household lending, which includes personal loans, fell 2.4 per cent in the month to $31.29 billion, 17.5 per cent lower than a year earlier. Lending to businesses jumped 10.8 per cent to $34.74 billion.  The financial regulator has called out the big banks for "unreasonably delayed" and in some cases "legalistic" fees-for-no-service reviews.

ASIC says Westpac, ANZ, NAB, Macquarie and AMP have yet to complete reviews of systemic fees-for-no-service failures beyond those already reported since 2013. That's despite the regulator advising them to conduct them in 2015 or 2016. Commonwealth Bank completed its further reviews but told the Australian Securities and Investments Commission in December it would look into whether three of its licensees had extracted fees-for-no-service. ASIC commissioner Danielle Press said the size of the reviews - which go back six to 10 years and cover 36 licensees from six institutions that currently authorise more than 7,000 advisers - did not excuse the sluggish response. 'These reviews have been unreasonably delayed," Ms Press said. "ASIC acknowledges that they are large scale reviews ... however, we believe the institutions have failed to sufficiently prioritise and resource their reviews." She said the main reasons for the delays included poor internal record keeping and inadequate methodologies such as some institutions proposing to make customers opt in to a review and remediation program. "Some institutions have taken a legalistic approach to determination of the services they were required to provide," Ms Press said. She welcomed the government’s commitment to give ASIC new directions powers that could speed up future remediation programs. The charging of fees for services that customers didn't need, couldn't access or didn't know they were entitled to was one of the major scandals heard by the financial services royal commission. While CBA is reviewing its three licensees, Macquarie estimates it will complete its review by mid 2019 and AMP in the second half of 2021. ANZ, NAB licensee JBWere and Westpac licensees Magnitude and Securitor have not given ASIC their proposed target dates for completion. AMP Capital has promoted Debbie Alliston to chief investment officer of its $62 billion multi-asset funds portfolio. Ms Alliston assumes the role from Sean Henaghan, who is taking a 15-month sabbatical. She will be responsible for teams within AMP Capital's multi-asset group delivering tailored investment including asset allocation and portfolio construction. AMP Capital invests funds on behalf of clients as well as AMP, and is managed independently to the AMP Group.  AMP Capital Global head of public markets Simon Warner said Ms Alliston is ideal for the position following seven years managing multi-asset portfolios.

"Debbie has an excellent understanding of the business and how we can execute our strategic priorities in a dynamic market," Mr Warner said on Thursday. Ms Alliston will report to Mr Warner, who was appointed head of its freshly formed public markets business from October last year. AMP Capital's parent company AMP recently reported full-year profit dropped 97 per cent, to $28 million, after the firm set aside millions in remediation for its wrongdoings following its royal commission drubbing. At 1221 AEDT, AMP shares were flat at $2.37.  Australia's competition watchdog has dropped a provisional date for when it will decide whether to approve TPG Telecom's proposed merger Vodafone Group Plc, an update on its website shows.

In its latest delay, the Australian Competition and Consumer Commission (ACCC) said on Friday it was still receiving required information from TPG and Vodafone before it can set a new provisional date for its decision on the mega-telco tie-up. ACCC had initially set a provisional date of March 28, but in January pushed that back by two weeks to April 11. In December, ACCC said it was concerned whether the merger would reduce the incentive for the resulting entity to offer lower prices, as the deal involves two of the industry's biggest four players. The regulator's decision may be further complicated by TPG's move in January to abandon plans to build a mobile telephone network due to a ban on the use of equipment from Huawei Technologies, its chosen supplier. A Vodafone spokesperson said the company has provided a "significant amount of material" already, and remains committed to the merger. TPG did not respond to an emailed request for a comment. |

RSS Feed

RSS Feed